Understanding Offset Accounts: A Key Strategy for Mortgage Savings

An offset account can be a good way to reduce the interest charged on your home loan, while also giving you access to your money whenever you need it. This article explains how offset accounts work, their benefits, and how you can make the most out of them.

What is an offset account?

An offset account is a transaction account linked to your home loan. You can make deposits or withdraw from it as you would with a regular transaction account.

The big difference is that when you hold money in an offset account over a period of time, you can reduce the amount of interest charged on your home loan. The higher the balance and the longer the period, the less interest you’ll pay. And this could help you pay off your loan sooner.

Generally speaking, the offset feature is only available on variable rate home loans (although some lenders offer an offset feature on selected fixed rate home loans).

How does an offset account work?

An offset account is a transaction or everyday banking account that is linked to your home loan. Every dollar you have in that account ‘offsets’ the interest of your loan – reducing the amount of interest you pay every month. Because these savings add up over time, you can also use this ‘extra’ money to pay your loan off faster.

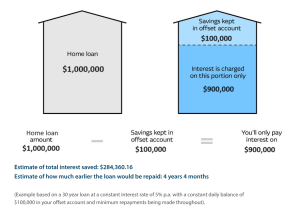

For example, if you have $100,000 in your offset account and home loan of $1,000,000. you’ll only be charged interest on $900,000.

How to use an offset account

Some people may have their pay deposited straight into their offset account and treat it as an everyday transaction account. Others may use their offset as a savings account for things like holidays or renovations – or for less exciting purposes like setting aside money for their tax bill.

Offset account Vs Normal savings account

Your money generally works harder in an offset account compared to a regular savings account. That’s because the interest rate you pay on a home loan is usually higher than the interest you earn in a savings account.

Another advantage is the interest you save by using an offset account won’t be considered income – which means it won’t be taxed. On the other hand, the interest you earn on a savings account will generally be considered income – and that means it may be taxed.

Offset accounts and savings accounts may have different fees and charges that apply.

Is an offset account right for you?

Everyone’s situation is different. Before deciding on a mortgage with an offset account, you may wish to consider a few factors. If you want regular access to your money, then an offset might work for you.

- Account Fees: Some offset accounts come with monthly or annual fees Or if your offset account is offered as part of a package, there’ll be an annual package fee.

- Loan Type: Not all mortgages are eligible for offset accounts.

- Discipline Required: Effective use requires keeping a healthy balance in the offset account. It may be worth considering whether the amount of interest you’re likely to save will be more than the fee

To sum up

- An offset account is a transaction account linked to your home loan.

- It could help reduce the amount of interest you pay on your loan and help you pay it off sooner.

- The more money in your offset account, the less interest you’ll pay.

If you have any questions or need personalized advice about offset accounts and how they can benefit your home loan, please don’t hesitate to reach out to us. Our team of experienced mortgage brokers is here to help you find the best financial solutions for your needs.

Disclaimer: This blog offers general information on mortgages and finance for informational purposes only. It is not a substitute for personalized advice from a qualified mortgage professional or financial advisor. Use your discretion and seek professional guidance based on your individual circumstances.